Fund information: unit linked plans in series 1, 2, 2a, 2b, 3, 3b & 7

The with-profits 90:10 fund shares out its profits and losses at a ratio of 90% to policyholders and 10% to Zurich. The fund invests in fixed and variable interest investments, shares, property and cash.

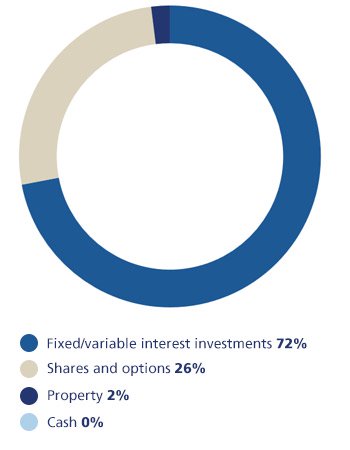

Asset Mix

Fund investment mix by value at 31 March 2026

The mix of investments varies between groups of plans and the investment mix for unit linked plans is shown here. The investment mix has not changed significantly in the 12 months to 31 March 2026 and there are no current plans to significantly change the investment mix in the future as we expect around 28% to remain invested in shares and property.

How did the funds perform in the 12 months to 31 March 2026?

The return achieved by the assets allocated to unit linked plans was:

- 8.0% before tax and charges for pension plans and

- 6.5% for life and investment plans before charges.

On average the charges for managing the fund were less than 0.7% of the fund’s value.

Previous performance figures

Before tax and charges

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|---|---|---|

| 8.7% | 9.8% | 0.5% | 9.9% | 2.2% | 2.5% | -9.9% | 8.8% | 3.9% | 9.8% |

| After tax | |||||||||

| 7.2% | 8.3% | 0.6% | 8.1% | 1.9% | 2.2% | -7.7% | 7.2% | 3.3% | 8.0% |

Current bonus rates

The rates below were declared on 12 January 2026.

Life Plans excluding Investment Bonds

| Fund Series | Regular Bonus | Current Final Bonus** |

|---|---|---|

| 2 EL | 3%* | 174% |

| 2a EL | 2.5%* | 343% |

| 2b EL | 2.5%* | 130% |

| 3 EL | 2.5%* | 313% |

| 3b EL | 2.5%* | 130% |

Investment Bonds

| Fund Series | Regular Bonus | Current Final Bonus** |

|---|---|---|

| 2 EL | 3%* | 186% |

| 3 EL | 2.5% | 241% |

Pension Plans

Series 1 EP (excluding Offshore version): The unit price for this series is calculated with reference to the value of the underlying fund so changes every day. The daily price also includes the adjustments made when valuing investment in other series by adding final bonuses or applying an MVR.

There is a guaranteed minimum price that applies on your selected retirement date and during 2026 it will increase by 3.0%. On 31 March 2026, the guaranteed minimum price was 429.7p compared to 1665.8p which is the price at which units were sold.

| Fund Series | Regular Bonus | Current Final Bonus** |

|---|---|---|

| Offshore 1 EP | 4%* | 97% |

| 2 EP | 4%* | 97% |

| 2a EP | 3.0%* | 254% |

| 2b EP | 3.0%* | 164% |

| 3 EP | 3.0%* | 224% |

| 3b EP | 3.0%* | 164% |

| 7 EP | 4%* | 97% |

* This includes the guaranteed rate of annual bonus.

** Final bonus rates are not guaranteed as they are periodically reviewed and changed from time to time (without notice) to ensure everyone receives their fair share of the fund's performance.

As the fund is closed, we aim to give all remaining investors a fair share of the estate (the part of the fund we use to help maintain bonus rates when returns are lower or to meet unexpected payments from the fund). For 2026, the final bonuses paid to investors leaving the fund will include an estate distribution of 95% of asset share, unless plan guarantees are higher. Note: This rate is not guaranteed and can change at any time which may cause significant changes in plan values.

We may reduce your plan value by applying a Market Value Reduction (MVR) if the regular bonuses we’ve added to your plan are greater than the smoothed return the fund achieved while you were invested in it - to make sure we only pay you your fair share of the fund.

Many plans have a date on which we guarantee not to apply any MVR and this date will be shown on your yearly statement.

While performance of the fund means we haven’t needed to apply MVRs since 2010 this may change in the future.

Information we send to customers

Bonus information is included with your yearly statement.

A copy of the leaflets, showing information about fund performance can be found through the following links:

Bonus leaflets for the year to:

How is the with-profits 90:10 fund managed?

The Principles and Practices of Financial Management’ (PPFM) shows how we manage the money in the with-profits 90:10 fund. This was last updated in January 2026.

How do I know you're managing the fund properly?

Zurich Assurance Ltd has to tell its with-profits policyholders each year if it has complied with its obligations in the PPFM (Principles and Practices of Financial Management). It does this through the annual report (last published June 2026, next issue due June 2027) from the board of directors, including a separate report from the with-profits actuary on Zurich Assurance Ltd's compliance with the PPFM. In preparing the report, the directors seek the view of the independent person.

It is the opinion of the board of directors that during 2025:

- the company has complied with its obligations in the PPFM

- the way discretion was exercised was appropriate

- competing or conflicting rights, interests or expectations were addressed in a reasonable and proportionate manner.

The report contains further information on this, particularly for bonus rates, investment strategy, surrender values, expenses and charges, changes to the PPFM and customer communications. (You may wish to refer to the PPFM for the definition of technical terms).

The board of directors have appointed Alison Carr to provide it with an independent assessment of compliance with the PPFM. Mrs Carr will also advise the board on how any competing or conflicting rights and interests of policyholders and shareholders have been addressed. This role is a senior manager appointment (SMF15) within the FCA’s Senior Managers and Certification Regime. The board have given Mrs Carr this Statement of Responsibilities for her role. The Statement of Responsibilities covers all aspects of the management of and the exercise of discretion in respect of the fund, including those matters which Rule 20.5.3 of the FCA’s Conduct of Business Sourcebook requires to be covered in a terms of reference.