Instalment changes explained

What is this information about?

We’re changing the type of premium finance agreements we use for monthly instalments by moving away from the running account model.

Our changed approach will mean that our new premium finance agreements will not be regulated under the Consumer Credit Act 1974 (“Act”). The Act allows for certain interest-free credit agreements to be entered into on an unregulated basis. The change in approach will mean that we can simplify the process, which will help us provide a quicker and smoother service for you. We’ll continue to provide the premium finance without any interest or charges.

Previously, where you are an existing customer, the financing of your insurance policy premium has been arranged through a running account credit agreement which is regulated by the Act.

For all new policies and renewals, we will no longer be offering financing of the premium under the running account credit agreement and instead we will offer a new unregulated fixed sum credit agreement for monthly instalments.

Customers who renew their insurance between 7 November 2025 and 31 December 2025 and are paying premium by way of monthly instalment

As noted above, at renewal of your insurance policy you will be offered financing of the premium under a new unregulated fixed sum credit agreement.

As your existing running account credit agreement has no fixed duration, it will continue to exist but will not be used for your premium. We will therefore be in touch separately after 31 December 2025 to formally end your running account credit agreement.

Customers who are due to renew their insurance on or after 1 January 2026

Your insurance policy premium is currently arranged through a running account credit agreement. You will receive a letter to let you know your instalments are being refinanced from a running account credit agreement to a fixed sum credit agreement with effect from 31 December 2025. The letter will contain the payment terms and loan agreement applicable to the new fixed sum credit agreement. If you choose to renew your insurance policy thereafter, you will be offered financing of the premium under a new unregulated fixed sum credit agreement.

Frequently asked questions

We have included some FAQs which explain the refinancing process and what this means for you.

Here’s how it works:

- You currently have an outstanding balance on your existing running account credit agreement (your existing agreement). This balance is paid monthly and covers the remaining insurance premium (including insurance premium tax) for your Zurich policy

- We’re asking you to enter into a new fixed sum credit agreement with us (your new credit agreement)

- This new credit agreement will replace your existing agreement

- When your new credit agreement is made, your existing agreement will end

- The amount of credit provided under your new credit agreement will be the same as what’s left to repay on your existing agreement for your Zurich insurance policy

The way we handle missed payments will not change; we will still tell you about the missing payments and give you time to pay the missing sum.

Yes. If you choose to repay early the loan in full or any part of the loan, you can do so with no additional charges or costs.

Your existing agreement is a running account agreement which has a credit limit which allows you to borrow money from time to time up to the credit limit. The credit limit is refreshed as you make payments.

Your new credit agreement is a fixed sum credit agreement which allows you to borrow a fixed sum of money over an agreed period of time. The fixed sum credit agreement will last for a maximum period of 12 months but it is likely to be less than that given the amount of credit being provided and the amount and number of repayments to be made.

Your existing agreement is regulated by the Consumer Credit Act 1974 (CCA) but your new credit agreement is not:

- The CCA gives a number of rights to information during the life of a credit agreement. This means some rights you have will no longer apply – for example, the right to certain information before you enter into the new credit agreement (and in the agreement itself) and the right to certain information during the life of the credit agreement, such as statements, default, arrears and termination notices

- However, we will still provide a statement of payments to you on request and will still tell you if you miss a payment or we are taking steps to end the credit agreement early. You will also still have a right to repay the credit early (in full or part) and you will have a right to cancel the credit agreement without giving a reason within 14 days of the credit agreement being made. You can also still complain to us if you are unhappy with the credit agreement or the way in which we are managing your account. The “unfair relationships” provisions in the CCA will also continue to apply

There are no changes to how you can end your new credit agreement.

There are some changes to how we can end your new credit agreement. We no longer need to send you a default notice where we have rights to end your new credit agreement; but we will continue to provide you with notice where payment is outstanding and we must now give you 28 days to make an outstanding payment after asking you to do so before we can end the agreement, before it was 14 days; and we no longer have the right to end your new credit agreement on two months’ notice.

The way we deal with your account on a day-to-day basis will not change. The number of payments that remain to be paid under your existing agreement will not change under your new credit agreement and the interest rate will remain at 0%. As noted above, the amount of your monthly payments will not change unless you have missed any payments under your existing agreement and these remain outstanding on 30 December 2025 (inclusive). If this is the case, please see question ‘What if I have defaulted under my existing agreement?’ below.

Please contact your broker who can contact us as required if you need any information on your payment terms.

Where you have missed any payments under your existing agreement and these remain outstanding on 30 December 2025 (inclusive), then the total amount of any such missed payments will be included in the total amount of credit under your new credit agreement, and it will be evenly distributed across the monthly payments under your new credit agreement. You or your broker may contact us to resolve any missed payments at any time, and to the extent they are repaid on or prior to 30 December 2025, then they will not be included in your new credit agreement. If you have any concerns with the proposed distribution of any missed payments under your new credit agreement, then you or your broker may also contact us to discuss options for managing repayment.

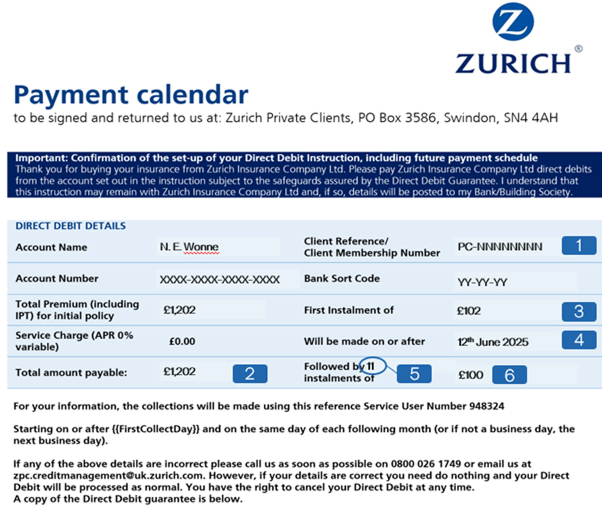

Below we have provided a working example of how to use the initial payment schedule for an existing running account credit agreement to understand the payment terms applicable to a new fixed sum credit agreement. Please see the notes in the letter sent to you outlining the refinancing as other documents may need to be considered as part of your review of the payment terms where you have, for example, made changes to your insurance policy or renewed since the initial payment schedule was sent to you.

Payment terms for your new credit agreement

Picture of initial payment schedule for your existing running account credit agreement:

- policy number

- total amount of credit

- first instalment

- first collection day

- number of instalments (excluding first instalment)

- instalment amount

Terms referred to in your new fixed sum credit agreement

Total amount of credit

This will be the total amount of credit which remains outstanding under your existing agreement as at 31 December 2025 (inclusive - including any missed repayments which remain outstanding).

You can calculate the amount by taking:

- the total amount payable shown on the latest payment schedule sent to you for your existing agreement (2) less

- any instalments you have made since the date that the latest payment schedule was sent to you and which you make up to 30 December 2025 (inclusive)

First instalment

This will be the first instalment amount shown on the latest payment schedule sent to you for your existing agreement and is referred to in this table. (3)

First monthly payment for the new credit agreement

This will be the same monthly instalment amount shown on the latest payment schedule sent to you for your existing agreement (but not the first instalment amount). (6)

First payment date and subsequent payment dates

This will be taken from 31 December 2025 onwards and will be the same day of the calendar month and the same day of each subsequent calendar month (or if not a business day, the next business day) as shown on the latest payment schedule for your existing agreement. (4)

Amount of subsequent monthly payments

This will be the same monthly instalment amount shown on the latest payment schedule sent to you for your existing agreement (but not the first instalment amount). (6)

Number of subsequent monthly payments

This will be the number calculated as follows:

- the number of instalments shown on the latest payment schedule sent to you for your existing agreement (but not the first instalment amount) (5) less

- the number of instalments which should have been made or which you should make according to the latest payment schedule from the date that the latest payment schedule was sent to you for your existing agreement (but not the first instalment amount) up to 30 December 2025 (inclusive) less

- the first monthly payment under your new credit agreement.

Calculating total amount of credit under the new agreement based on the illustration above

£1,202 (2) - (£102 (3) + 6 x £100 (6)) = £500

This is the total amount payable (2) less the sum of the payments from 12th June (4) to 12th December inclusive.

Calculating number of subsequent Instalments based on the illustration above

11 (5) - 6 (all payments from 12th July)* = 5

This is the total number of subsequent payments (5) less the number of payments made from 12th July to 12th December inclusive.

Key differences between running account and unregulated fixed sum agreements

| Running account credit agreement | Unregulated fixed sum credit agreement |

|---|---|

This has a credit limit which allows you to borrow money from time to time up to the credit limit. The credit limit is refreshed as you make payments. |

This allows you to borrow a fixed sum of money over an agreed period of time. The fixed sum credit agreement will last for a maximum period of 12 months but it is likely to be less than that given the amount of credit being provided and the amount and number of repayments to be made. |

Regulated by the Consumer Credit Act 1974 (CCA) and Zurich requires FCA authorisation for consumer credit activity. |

Exempt from the CCA and not subject to FCA authorisation. Whilst the credit agreement is not regulated, Zurich remains regulated by the FCA and has responsibilities under Consumer Duty to ensure your policy is fair value. We include consideration of the way you pay for your premium as part of that assessment. The ‘unfair relationships’ provisions in the CCA will also continue to apply. |

The CCA gives you rights to receive certain information before you enter into the new credit agreement (and in the agreement itself) i.e. pre-contract consumer credit information (PCCI). It also gives you the right to certain information during the life of the credit agreement, such as statements, default, arrears and termination notices. |

We will continue to send you the information you need to know regarding your credit agreement. This includes:

|

The agreement provides you with a right to withdraw within 14 days of the agreement being made and the right to repay early (in full or part) without penalty. |

You will continue to have the following under the terms of the new credit agreement:

|