UK industry set to miss 2050 net zero without urgent action

For further information please contact:

Emily Goodbrand Dillon

emily@thirdcity.co.uk

07879 815308

Victoria Dickson

vicd@thirdcity.co.uk

07719 939 901

22 September 2021

- Significant steps by government and widespread public behaviour change required for UK industry to hit 2050 carbon targets - University of West England

- Industry emissions reductions set to be just 40% of required levels by 2035

- Study of 17 UK industry sectors show majority are off track to hit Net Zero, with manufacturing, construction and transport facing greatest challenges

- Carbon colour-coding on food, supporting sustainable transport and ensuring consistent incentives to support low carbon technologies are among the potential solutions highlighted in the study

The majority of UK industry sectors will miss 2050 Net Zero targets unless there are significant further steps taken by government, including acceleration of consumer education and behaviour change.

This is according to the Journey to Net Zero report, commissioned by insurer Zurich UK and undertaken by the University of the West of England. The study examines the 17 key UK industry sectors, outlining the scale of their Net Zero challenge (table 1) and the steps that could help them play catch-up on carbon emissions. It acts as an extension to Zurich’s global white paper on climate challenges – Closing the Gap on Climate Action.1

Most of the 17 industry sectors are currently off track to hit 2050 emissions targets, given they are expected to miss 2035 emission reduction targets by 197 megatons (131mt reduction, of a required 328mt).2 The report identifies manufacturing, construction and transport as needing particular attention given the steep carbon challenges they face. The report found that only five of the 17 industries analysed are currently decreasing emissions, five are stable and seven are actually increasing their levels of emissions year on year.3

Government action required

The study highlights the interconnections that exist between industry sectors, necessitating Government to act as the coordinating voice in order to implement progressive initiatives.

This is particularly relevant for some heavy industries within manufacturing. For example, carbon-intense cement production impacts the construction sector directly. This means that many industry’s challenges can’t be overcome without the adoption of a ‘whole of supply chain’ perspective.

Some tasks are also too great for any one industry and require a nationwide approach, including the education of consumers and enabling behaviour change to make greener options more desirable.

Challenges and possible solutions

In addition to the need for clear incentives for low carbon technology and a more consistent approach to data, the report also highlights some industry-specific challenges.4

While some industries could initiate solutions themselves, assistance from the government was highlighted as preferable, if faster progress is desired.

These include:

- Accommodation and food services. Key challenges: Minimise waste and encourage more environmentally conscious choices. Possible solutions: Carbon colour coding for food products akin to nutritional traffic light system.

- The Construction and Real Estate industries face a major challenge in both making new builds greener and reducing emissions from our existing housing stock. Stricter building standards would make building less carbon-intensive and a large-scale nationwide retrofitting scheme for poor performing appliances could also help, although would take significant time to implement and require consumer incentives.

- IT & Communication. Key challenge: The sector produces too much technology waste, which requires a step change in the way we source technology – building circular economy practices into procurement processes. The report noted that use of technology would be crucial in other sectors reducing emissions by allowing comprehensive remote working.

The report strongly recommends focusing on enabling a shift in public attitudes in addition to finding technological solutions, and highlights the arts and entertainment sector as having a key role to play in influencing public opinion, encouraging responsible consumption and understanding what’s at stake for the earth.

At what cost?

The report underlines that although the cost of decarbonisation will reach 1-2% of GDP in 20505, it is ultimately affordable - and the cost of inaction will be far greater. It’s made clear that such costs don’t take into account significant secondary financial benefits of a lower carbon economy, such as improved air quality reducing cost to the NHS.

Crucial policy changes and investment

The report suggests where investment is needed in large scale infrastructure and technology ventures, as well as where more work is required to educate consumers and drive behaviour change (e.g. consumption or travel habits).

A task identified as too great for any one industry is standardised carbon accounting which needs to properly reflect supply chain interdependencies - i.e. the whole of the life cycle of products.

Zurich UK is also calling on the Government to improve access to carbon capture and storage for all sectors, particularly those identified in the report as having an opportunity to benefit significantly from this technology.

Shaun Hicks, Chief Risk Officer at Zurich UK said:

“The Government needs to publish a detailed roadmap to a net-zero economy, with sector-by-sector analysis and a timeline of decarbonisation expectations to contribute to the overall 2050 national target. Whilst the application of innovations such as hydrogen fuel and carbon capture have great potential in realising a green future, the government needs to provide further clarity to give businesses the time they need to prepare for the net-zero transition.

“This study underlines that certain sectors are going to find it tough to decarbonise. Yet despite this, it’s also clear that there are sustainable actions which every business and individual can do now to contribute to the progress we need to achieve net zero by 2050.”

Dr Laura de Vito, lead report author from the University of the West of England Faculty of Environment and Technology said:

“The UK industrial sectors are highly interconnected and therefore it is important to adopt a joined-up and collaborative approach to Net Zero. “Solutions are available - we now must focus our efforts in implementing them, especially in light of the recent IPCC report which demands urgent and decisive change.

“The UK government will need to play a crucial role in driving this change at the required scale and pace, and in unlocking collaboration opportunities across industry sectors and at all levels of society.”

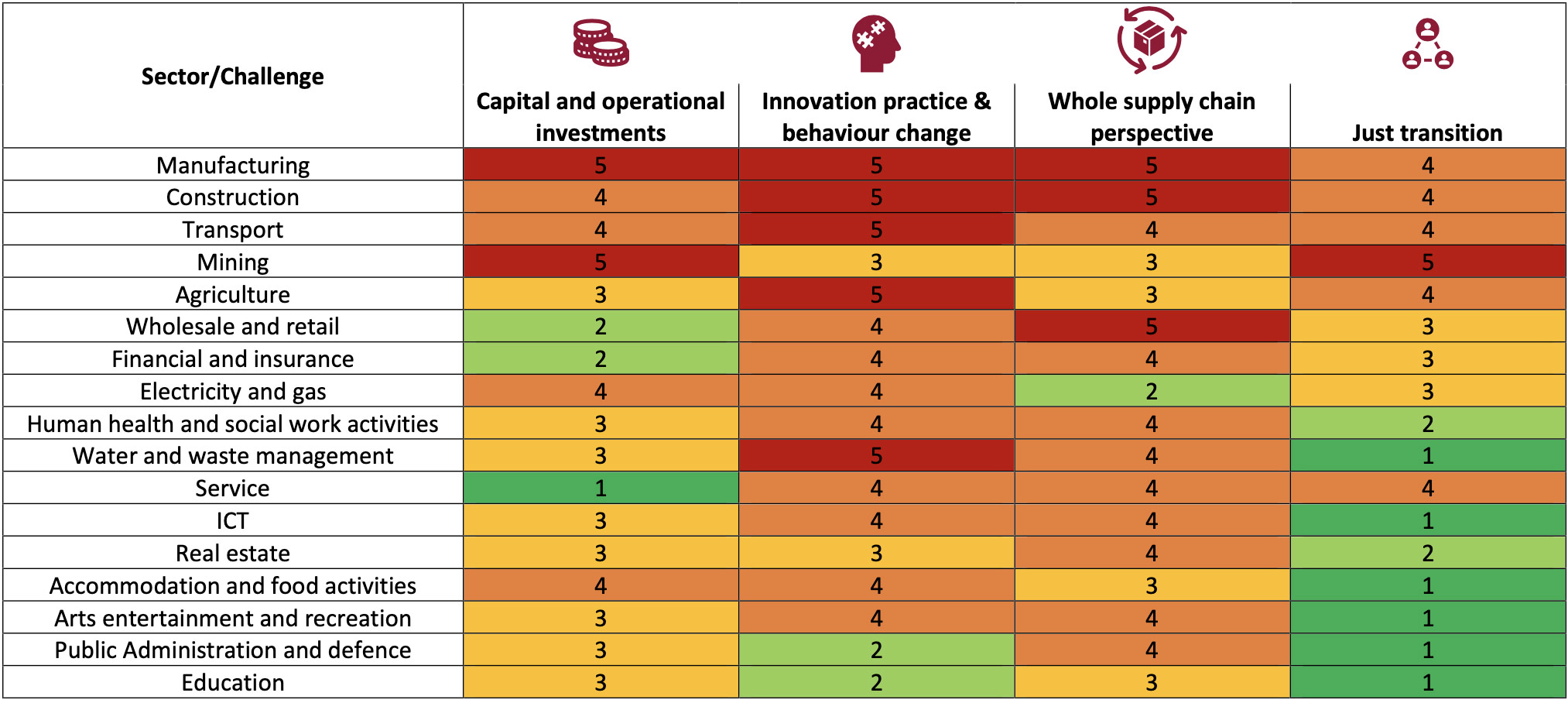

Table: Sectors and challenges identified by the report in a ranked grid4

Report methodology

Each of the 17 UK Standard Industry Categories (SIC) were audited using a wide range of scientific and government literature with a broad increasing/stable/decreasing trend marked against each. In addition, the scale of each industry’s challenge was outlined by scoring across four sub-categories (1. Reducing cost 2. Innovation and behaviour change 3. whole of supply chain challenge 4. Just transition challenges). Further methodology clarification detailed in full report (available upon request).

Footnotes

1. Full report Closing the Gap on Climate Action

2. Data taken from UK Climate Change Committee 2021 Report to Parliament, 2035 GHG emissions reductions required is 328mt. Currently the UK is on track to reduce by just 131mt (based on 2009-2019 trends), leaving us 197mt short by 2035

3. Increasing: Water and waste, Construction, Transport, Real Estate, Wholesale & retail, Agriculture & food. Stable: Mining, Manufacturing, ICT, Financial services, Professional/Scientific/Technical. Decreasing: Energy, Public admin & defence, Education, Health, Arts.

4. Breakdown of challenges identified in the report (more detailed breakdown can be found in the report itself):

- Capital and operational investments – the challenge for sectors of gaining financing for investing in Net Zero solutions and infrastructure, and reversing entrenched practices

- Innovation practice and behaviour change – the challenge faced by a lack of sector knowledge of low-carbon alternatives, as well as a lack of good quality benchmark data and effective innovation

- Whole supply chain perspective – the challenge of dealing with emissions that are embedded in the entire sector supply chain, beyond just the emissions generated by the specific products or services being produced

- Just transition – the job-loss challenge faced by sectors moving to a low-carbon structure, particularly where they are focused in a single UK region

5. Data from UK Climate Change Committee